One thing that hit me about LTCM’s failure is this: they failed not because their models were wrong, but because they ran out of capital. I came across a simple mathematical example of a strategy which illustrates a strategy that runs out of capital and will share it with you.

The double or nothing strategy

We consider a discrete time market which is both fair and efficient. There is, however, a way of making a guaranteed profit. What is the catch? You need an infinite amount of capital.

Consider the shares of Fairness Company. The company has an equal (and independent) chance of doing well (in which case the share price goes up) or poorly (in which case it falls) every period. We take out a derivative which pays 2 if the shares go up and 0 if they go down in the next time period. Naturally, the cost of one unit of this derivative is 1, the expected gain. So if we buy one unit of this derivative we will make a profit of 1 with probability ½ and a loss of 1 with probability ½. The expected profit is zero.

Let us call the profit on the derivative at time t (which we buy at time t-1) dt. So

Suppose we hold Yt units at time t, which we buy at time t-1 and we start off by buying one derivative. So with probability ½ we gain or lose Yt units at each period. Our accumulated loss/gain at time n is then

If the share goes up after the first period, we stop and get a profit of 1. If it goes down we bet more, so that when the share does go up we recover our loss and make a profit. That is we invest 1 (our original holding), plus what we lost, also 1. So we invest 2.

So we set

It is important that Yn depends only on n-1, which is something we already know when we buy our next set of derivatives.

Note that if dn = 1 then

and Yn = 0. So we naturally stop when we make a profit.

If we do not make a profit, but a loss, we get

So for our next bet we need to invest

So after each period we double our bet, as long as we are losing. Let us call the time when we stop T.

T is finite with probability 1. Which can be seen because

Adding up for all n gives

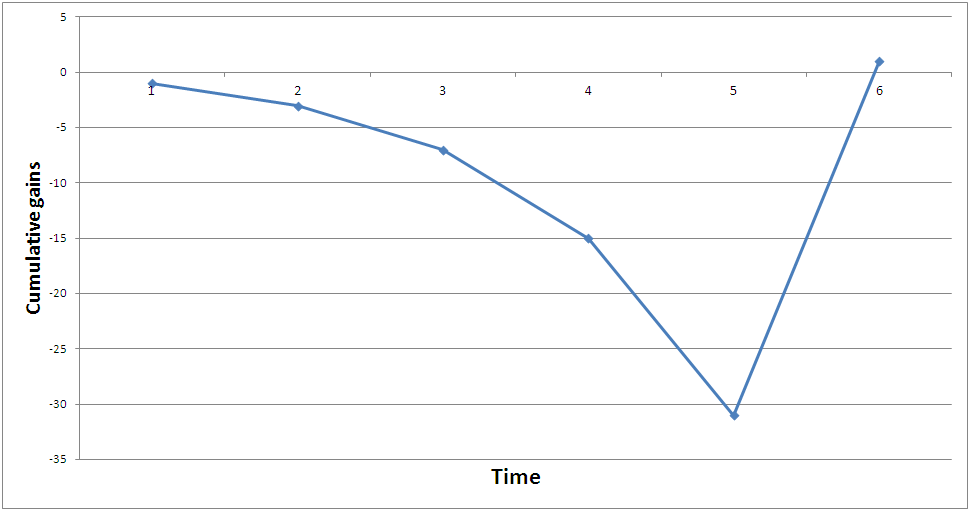

So eventually the strategy will stop and you will get your guaranteed reward of 1. An example of how this happens is shown in the following graph. Note how large your losses become before you eventually make your (by that time miniscule) profit.

But how much money should you have, exactly?. Well your last bet has value

and the expected amount you need, just for this last bet, is then

The moral

This example is, of course, very simple and somewhat contrived. It does illustrate one salient point: A strategy that must “eventually” work can fail if you cannot stay solvent long enough to see it through.

In this case the problem is, of course, that the market is fair. If markets actually are fair you cannot beat them. Another reason your strategy may fail is because of market irrationality. The market may be completely irrational in the short term. LTCM was waiting, quite reasonably, for the prices of Royal Dutch and Shell to converge (they WERE shares in the same company after all). However, they just did not have the ability to wait long enough.

Doubling your bet at each period may seem insane, but there are many investors out there who believe that if a stock they hold goes down, this is a sign to buy even more of it as it is now even more undervalued. Of course, if markets are mean-reverting and the stock truly is undervalued then this may be legitimate.

The problem comes when you borrow in order to buy the stock, then you may be expected to repay your debt before your profits have come. And no one has unlimited borrowing capacity.

Never devise a strategy without considering how much capital you might need. Never assume that you will not need to make a (dis)graceful exit. I leave you with the words of John Maynard Keynes, whose wisdom mocks us even today:

"Markets can remain irrational a lot longer than you and I can remain solvent."

Some references

- Spreij, P. J. C. (2011). Measure Theoretic Probability. Retrieved from http://sites.google.com/site/mtp1112/mtp.pdf?attredirects=0

- Wikipedia. (2011). Long-Term Capital Management. Wikipedia. Retrieved from http://en.wikipedia.org/wiki/LTCM